Why should restoration companies price by job type? Different restoration job types — water mitigation, fire remediation, mold, reconstruction, contents, biohazard — have different labor profiles, equipment utilization, documentation loads, and payer mixes. A single blended margin across all of them averages the profitable work against the unprofitable work and hides which categories are actually contributing. Pricing and margin discipline managed by job type surfaces the truth and makes strategic decisions possible.

A restoration company doing $5 million a year reports a 38 percent gross margin for the trailing twelve months. The owner is satisfied with the number. The business looks healthy at the aggregate.

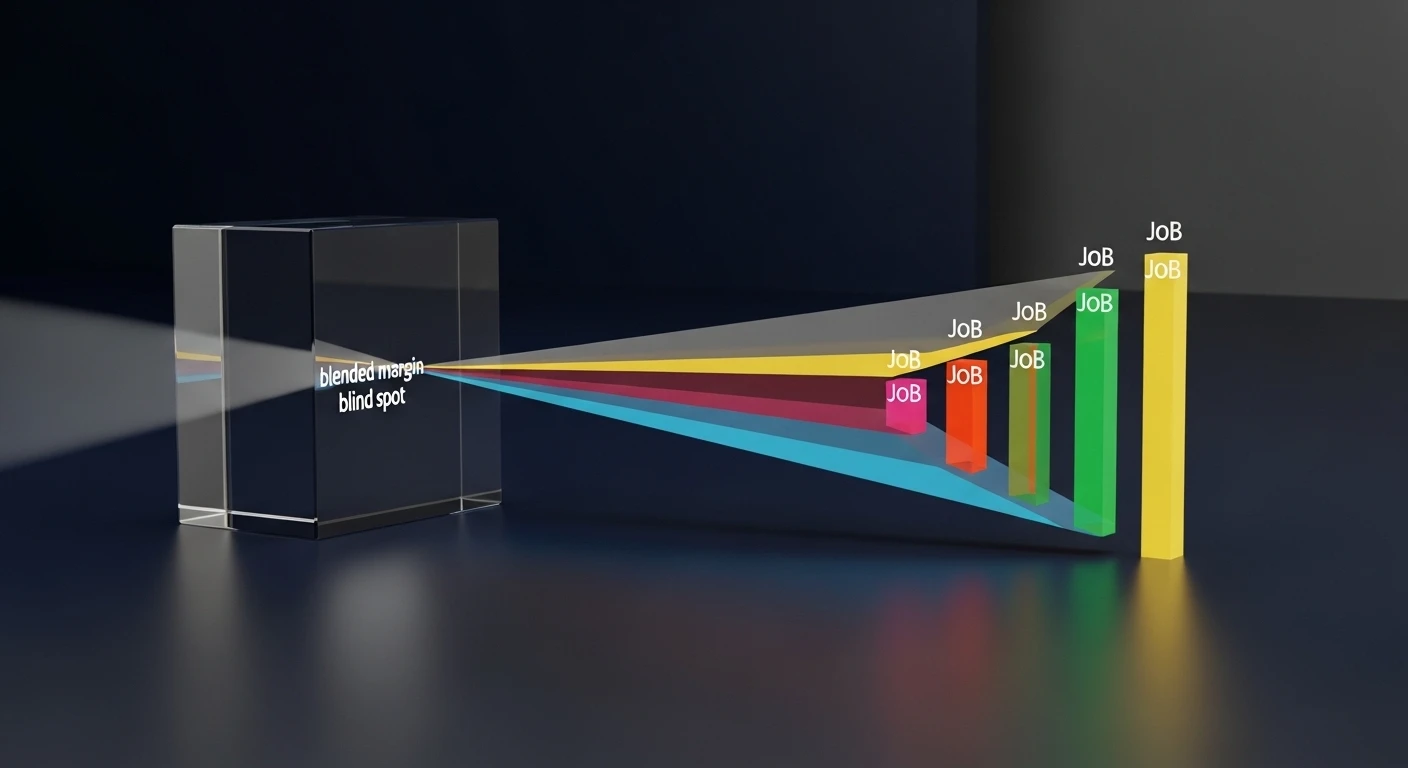

The aggregate is the wrong lens. Underneath that 38 percent is a 52 percent margin on emergency water mitigation, a 41 percent margin on contents, a 29 percent margin on reconstruction, an 18 percent margin on certain TPA-program fire work, and a negative-margin category of mold remediation that the company has been taking on because it feels like the full-service thing to do. The blended number is a math average of all of them. The business is not evenly healthy — it is one category propping up two others, and the owner cannot see it because the margin lens is aggregate.

This is the blind spot that pricing-by-job-type solves.

Why Blended Margin Hides the Truth

Blended margin is a single number that averages the economics of every category of work the company does. When the categories have genuinely different cost structures — and in restoration they almost always do — the blended number describes none of them accurately.

Water mitigation has a predictable labor profile, standardized equipment deployment, clean documentation paths, and historically healthy payer response times. It tends to run at the higher end of a restoration company’s margin range.

Fire remediation has longer job durations, more specialized labor, higher equipment loads, and more complex documentation. It often runs at different margin levels than water — sometimes higher because of the premium pricing, sometimes lower because of the scope complexity.

Mold remediation has narrow-specialty labor, containment protocols that drag productivity, and documentation requirements that vary by jurisdiction. Margin can be attractive with the right pricing and controlled with the wrong pricing.

Contents cleaning and storage is a different business inside the business — labor-intensive, inventory-heavy, documentation-heavy, and often priced differently than the structural work attached to the same claim.

Reconstruction is the category where most restoration companies see margin compress. Longer cycle times, more subcontractor exposure, harder documentation, scope drift risk. A company that priced mitigation on a clean system can still bleed on reconstruction if the pricing model does not reflect the different economics.

Blended margin averages these. Pricing by job type treats each as its own economic unit.

What Pricing by Job Type Actually Requires

Pricing by job type is not just “different rates for different work.” It requires that the company can answer three questions for each category:

What is the fully-loaded cost structure of this job type? Labor at burdened rate, materials, equipment at allocated rate, subcontractors, plus the overhead allocation covered in the overhead article.

What is the typical payer mix and payment cycle for this job type? A job type dominated by fast-paying payers has different economics than one dominated by slow-paying programs, even at the same nominal margin.

What is the variance profile on estimates versus actuals for this job type? Categories with high variance need higher margin cushion because the downside risk on any given job is larger.

Once those three questions are answered, the pricing model for each category can reflect its specific economics — target margin, pricing bands by scope size, acceptable payer programs, risk-adjusted cushion. The company is no longer pricing every job against a single blended target.

The Strategic Decisions That Emerge

When pricing and margin are managed by job type, strategic decisions sharpen.

Service line investment. The company can tell which categories produce the strongest fully-loaded return on invested capital. Growth investment gets directed there rather than distributed evenly across categories.

Program acceptance. A TPA program that looks attractive on rate can be evaluated against the specific job type it feeds. If the program sends primarily reconstruction work at rates that are already thin on reconstruction, the fully-loaded math might show a dilutive program even at attractive topline revenue.

Pricing adjustment. Categories where margin has drifted become identifiable. The estimator drift covered in the job costing article is easier to correct when the drift is visible by category rather than absorbed into a blended average.

Training and capability investment. When the company knows which job types drive the highest return, training and equipment investment can be directed to strengthening those categories rather than spread thin across all of them.

Acceptance discipline. Some categories at some pricing points stop making sense. Being able to see that clearly — with the data to support the conversation — is what enables the company to decline work intentionally rather than accept everything and hope the averages work out.

The Common Pattern: One Category Subsidizing Another

Almost every restoration company that installs pricing-by-job-type finds the same pattern: one or two categories are carrying the math, one or two are running on mediocre margin, and one is quietly losing money.

The losing category is usually one of three things. A legacy service line the company continued out of habit after the market shifted. A TPA-driven category where the rate structure has compressed below the cost structure but no one ran the math. A new service line that was added on a revenue argument rather than a contribution argument and has not been evaluated since.

Finding it is not a comfortable discovery. Acting on it — adjusting pricing, renegotiating programs, exiting certain categories, or retooling the economics — is the work that actually improves the business. The pattern only becomes visible when margin is segmented by job type.

What the Report Should Look Like

The operating report that supports pricing-by-job-type is a rolling twelve-month view segmented by category, with several columns per category:

- Revenue (trailing 12 months)

- Number of jobs

- Average revenue per job

- Gross margin (fully-burdened labor, materials, equipment, subs)

- Overhead allocation

- Fully-loaded margin

- Average days to payment

- Working capital cost at the company’s effective rate

- Net contribution after working capital cost

The last column is the number that matters most. A category with a 35 percent fully-loaded margin that takes 150 days to collect at a 10 percent working capital cost is contributing a different net number than a category with a 32 percent margin that collects in 45 days. The comparison is not obvious from margin alone.

This report should be reviewed at least quarterly by the owner and the finance function, with specific pricing and strategic decisions coming out of each review.

The Pricing Band Framework

Pricing by job type does not mean a single rate per category. It means a pricing band — a target margin with defined acceptable ranges and defined override rules.

For a category with strong economics and low variance, the band might be narrow (target margin ±3 points). For a category with higher complexity or variance, the band is wider (±6 or 8 points) with specific criteria for where in the band a given estimate should land.

Estimates that fall below the band require documented justification and approval per the tiered approval article. Estimates that fall above the band may signal either premium opportunity or unrealistic expectations — both worth flagging.

The band framework is what converts pricing-by-job-type from a concept into an operating discipline.

How This Pairs With the Post-Mortem

Pricing-by-job-type and the every-job post-mortem reinforce each other directly.

The post-mortem looks backward at the actual margin produced on closed jobs. Segmented by category, those actuals feed the pricing model for future jobs in the same category. Categories drifting downward on actuals drive pricing adjustments. Categories consistently beating target drive investment in that capability.

Without pricing-by-job-type, the post-mortem’s margin observations do not have anywhere to flow. With it, every post-mortem closes the loop into pricing discipline.

Where to Start

If your company is operating on a blended margin view today, segment this quarter.

Identify the five or six job categories that represent the bulk of your revenue. Pull the last thirty closed jobs in each category. Calculate fully-loaded margin by category. Add average days to payment. Calculate working capital cost per category using your bank rate or a reasonable estimate of your cost of capital. Rank the categories.

The ranking will tell you something you did not know before. Use it to drive the next pricing decisions, the next program acceptance decisions, and the next capacity planning conversation.

Build the report into a quarterly cadence. Update the pricing bands annually. Over twelve to twenty-four months, the margin trend of the business reflects the discipline — not because anything dramatic happened, but because strategic decisions stopped being made on the wrong lens.

Frequently Asked Questions

What is pricing by job type in restoration?

The practice of managing target margin, pricing bands, and acceptance criteria separately for each category of restoration work — water mitigation, fire, mold, reconstruction, contents, biohazard — rather than applying a single blended margin target across all work.

Why is a blended margin number misleading?

Because different restoration job types have genuinely different cost structures, cycle times, and payer mixes. A blended number averages profitable categories against unprofitable ones and hides which categories are actually contributing and which are dilutive.

What categories should restoration companies track separately?

At minimum: water mitigation, fire remediation, mold, reconstruction, contents cleaning and storage, biohazard or specialty remediation, and major category variants (commercial large loss, for example). Company-specific categories may also warrant separate tracking.

What is a pricing band?

A target margin with defined acceptable ranges for estimates. Estimates within the band require no special approval; estimates below the band require documented justification and higher-level sign-off per the company’s tiered approval policy.

How often should pricing-by-job-type be reviewed?

Actuals by category should be reviewed at least quarterly. Pricing bands and category strategy should be reviewed at least annually. Fast-growing companies or those with shifting payer mix may want more frequent review.

What if a category shows negative fully-loaded margin?

The options are: raise pricing if the market allows, improve cost structure on that category, renegotiate program terms if the category is program-driven, or exit the category. The right answer depends on strategic fit, capability cost of exit, and the opportunity cost of the resources the category consumes.

Tygart Media on restoration — an analyst-operator body of work on the systems that separate compounding restoration companies from busy ones. No client names. No brand placements. Just the operating standard.

Leave a Reply